In the intricate landscape of insurance, the choice between claims-made and occurrence policies can significantly impact how coverage is triggered and claims are handled. Understanding the nuances of these policies is crucial for both insurers and the insured. Let's delve into the key aspects of occurrence and claims-made coverage triggers, exploring their differences and implications.

Occurrence Coverage Trigger

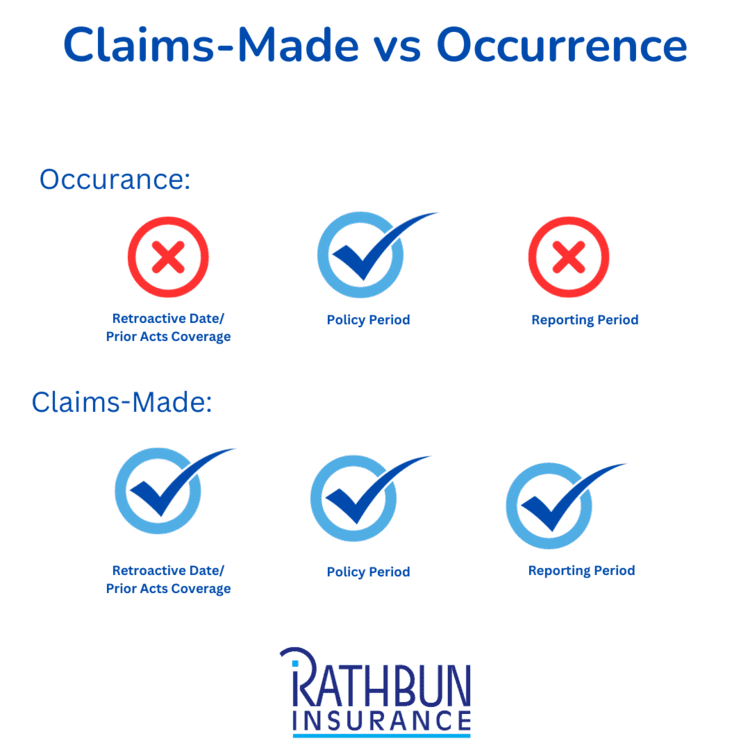

Defining Occurrence Policies: An occurrence policy is activated by a covered event, often referred to as an occurrence. This could be an incident resulting in bodily injury (BI) or property damage (PD) during the policy period. The policy covers claims arising from such events, regardless of when they are reported. For example, if an injury occurs during the policy period, the claim is covered even if reported after the policy expires.

Open-Ended Nature and Challenges: Occurrence policies present a challenge for insurers due to the difficulty in estimating ultimate losses. Claims might surface decades after the policy expiration, posing a unique challenge for both insurers and the insured.

Retroactive Dates: These policies necessitate that the policy is in force when the BI, PD, or personal and advertising injury (PAI) occurs. Discontinuing operations and canceling the policy leaves the insured without liability protection for subsequent incidents.

Claims-Made Coverage Trigger

Understanding Claims-Made Policies: In contrast, a claims-made policy is triggered by the making of a claim during the policy period or the Extended Reporting Period (ERP). There are two primary types: Claims-Made and Reported, and Pure Claims-Made.

Key Differences: Claims-Made and Reported policies demand that the claim be both made and reported during the policy period or ERP. Pure Claims-Made policies, however, have a less stringent reporting requirement, allowing claims to be reported as soon as practicable.

Retroactive Dates in Claims-Made Policies: A crucial element of claims-made policies is the retroactive date, limiting coverage to incidents occurring after a specified date. Claims arising from events before this date are not covered, emphasizing the importance of understanding policy details.

Extended Reporting Period (ERP): To address claims made after the policy expires for incidents during the policy period, an ERP, or tail coverage, is crucial. It provides a window for reporting claims after the policy expiration, ensuring continued protection for incidents before the policy ended.

Trigger Theories and their Impact

In complex claims involving multiple defendants and latent BI or PD, determining the trigger theory becomes pivotal. Four major trigger theories guide the determination of when coverage is activated:

- Exposure Theory: Triggered by the first exposure to harmful conditions.

- Manifestation Theory: Triggered when the claimant becomes aware of the injury or damage.

- Injury-In-Fact Theory: Activated by the date BI or PD actually occurs.

- Continuous or Triple Trigger Theory: Triggered by initial exposure, actual occurrence, or manifestation.

These trigger theories influence the development of insurance policies and their application varies across states and jurisdictions.

Conclusion: Navigating the Insurance Maze

Choosing between claims-made and occurrence policies requires a careful evaluation of the specific needs and risks of the insured. Insurers and insured parties must collaborate closely to comprehend the coverage triggers, reporting requirements, and potential gaps in protection. In the ever-evolving landscape of insurance, knowledge is the anchor that ensures smooth sailing through the complexities of claims and coverage.